#Underground Mining Equipment Market share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 27% of US Tumblr users had an annual household income of over $100,000.

Text

Coal Handling Equipment Market Industry Analysis and Forecast By 2028

The Coal Handling Equipment Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2028. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Coal Handling Equipment Market:

The global Coal Handling Equipment Market is expected to experience substantial growth between 2024 and 2031. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-coal-handling-equipment-market

Which are the top companies operating in the Coal Handling Equipment Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Coal Handling Equipment Market report provides the information of the Top Companies in Coal Handling Equipment Market in the market their business strategy, financial situation etc.

thyssenkrupp; FLSmidth; Metso Corporation; Kawasaki Heavy Industries, Ltd.; FAM GmbH; IHI Corporation; Elecon Engineering Company Limited; Sumitomo Heavy Industries Material Handling Systems Co.,Ltd.; TAKRAF GmbH; FAMUR SA; AUMUND Fördertechnik GmbH; TRF Limited; GMV Engineering.; Atlas Copco (India) Ltd.; Hitachi Construction Machinery Europe NV.; Caterpillar.; Aesha Conveyors And Crushing Equipment.; FAB 3R; Dynamic Air Inc.; Sterling Engineering Co.

Report Scope and Market Segmentation

Which are the driving factors of the Coal Handling Equipment Market?

The driving factors of the Coal Handling Equipment Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Coal Handling Equipment Market - Competitive and Segmentation Analysis:

**Segments**

- On the basis of type, the global coal handling equipment market can be segmented into material handling equipment, crushing equipment, and screening equipment. - Based on application, the market can be categorized into surface mining, crushing, pulverizing & screening, and underground mining.

**Market Players**

- Some of the key players operating in the global coal handling equipment market include Caterpillar Inc., Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Volvo Construction Equipment, Sandvik AB, Metso Corporation, FLSmidth & Co. A/S, and thyssenkrupp AG. - Other prominent companies in the market are Terex Corporation, P&H Mining Equipment Inc., CNH Industrial N.V., SANY Group, and Eickhoff GmbH.

The global coal handling equipment market is anticipated to witness significant growth by the year 2028. The rise in coal mining activities across various regions, coupled with the increasing demand for coal in industries such as power generation and steel production, is expected to drive the market. The material handling equipment segment is likely to dominate the market during the forecast period, given its crucial role in efficiently transporting coal from mines to processing plants or end-users. The crushing equipment segment is also set to experience substantial growth, as it plays a vital role in reducing the size of coal for easier handling and processing.

In terms of applications, the surface mining segment is projected to hold a considerable market share, driven by the growing adoption of surface mining techniques due to their cost-effectiveness and efficiency in extracting coal from shallow deposits. The crushing, pulverizing & screening segment is also expected to witness robust growth as these processes are essential for preparing coal for various industrial applications. Moreover, the underground mining segment is likely to grow steadily, supported by the utilization of advanced coal handling equipment to ensure safety and productivity in underground mining operations.

Key market players such as Caterpillar Inc. and Komatsu Ltd. are focusing on product innovations and strategic collaborations to strengthen their market presenceThe global coal handling equipment market is poised for substantial growth in the upcoming years, primarily driven by the steady increase in coal mining activities worldwide. The demand for coal in key industries such as power generation and steel production remains robust, propelling the need for efficient coal handling equipment. The material handling equipment segment is expected to lead the market, as it plays a critical role in the seamless transportation of coal from mines to processing plants or end-users. This segment's dominance is further supported by the rising focus on operational efficiency and cost-effectiveness in coal handling processes.

Additionally, the crushing equipment segment is anticipated to witness significant growth due to its essential function in reducing the size of coal, making it easier to handle and process. As industries aim for better productivity and operational efficiency, the adoption of advanced crushing equipment is likely to increase. Moreover, advancements in technology and innovative solutions in crushing equipment are expected to further drive market growth and provide enhanced capabilities for coal processing operations.

In terms of applications, the surface mining segment is slated to hold a substantial market share, fueled by the increasing preference for surface mining techniques for their cost-effectiveness and high efficiency in extracting coal from shallow deposits. The ease of access to coal reserves through surface mining methods is a key factor contributing to the segment's growth. Additionally, the crushing, pulverizing & screening segment is poised for robust expansion as these processes are essential for preparing coal for various industrial applications, ensuring the quality and consistency of the final product.

Furthermore, the underground mining segment is expected to exhibit steady growth supported by the deployment of advanced coal handling equipment to enhance safety and productivity in underground mining operations. Players in the market such as Caterpillar Inc., Komatsu Ltd., and Hitachi Construction Machinery Co., Ltd. are actively engaged in product innovations and strategic partnerships to strengthen their market presence and cater to the evolving needs of the coal handling equipment industry. Collaborations with technology providers and a focus on enhancing equipment efficiency and durability are key strategies adopted by these market players to maintain a competitive**Market Players:**

- thyssenkrupp - FLSmidth - Metso Corporation - Kawasaki Heavy Industries, Ltd. - FAM GmbH - IHI Corporation - Elecon Engineering Company Limited - Sumitomo Heavy Industries Material Handling Systems Co., Ltd. - TAKRAF GmbH - FAMUR SA - AUMUND Fördertechnik GmbH - TRF Limited - GMV Engineering - Atlas Copco (India) Ltd. - Hitachi Construction Machinery Europe NV. - Caterpillar - Aesha Conveyors And Crushing Equipment - FAB 3R - Dynamic Air Inc. - Sterling Engineering Co.

The global coal handling equipment market is poised for substantial growth in the upcoming years, primarily driven by the steady increase in coal mining activities worldwide. The demand for coal in key industries such as power generation and steel production remains robust, propelling the need for efficient coal handling equipment. The material handling equipment segment is expected to lead the market, as it plays a critical role in the seamless transportation of coal from mines to processing plants or end-users. This segment's dominance is further supported by the rising focus on operational efficiency and cost-effectiveness in coal handling processes.

Additionally, the crushing equipment segment is anticipated to witness significant growth due to its essential function in reducing the size of coal, making it easier to handle and process. As industries aim for better productivity and operational efficiency, the adoption of

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Coal Handling Equipment Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Coal Handling Equipment Market, expected to exhibit impressive growth in CAGR from 2024 to 2028.

Explore Further Details about This Research Coal Handling Equipment Market Report https://www.databridgemarketresearch.com/reports/global-coal-handling-equipment-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Coal Handling Equipment Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Coal Handling Equipment Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Coal Handling Equipment Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2031) of the following regions are covered in Chapters

The countries covered in the Coal Handling Equipment Market report are U.S., Canada and Mexico in North America, Brazil, Argentina and Rest of South America as part of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe in Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA

Detailed TOC of Coal Handling Equipment Market Insights and Forecast to 2028

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Coal Handling Equipment Market Landscape

Part 05: Pipeline Analysis

Part 06: Coal Handling Equipment Market Sizing

Part 07: Five Forces Analysis

Part 08: Coal Handling Equipment Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Coal Handling Equipment Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Japan: https://www.databridgemarketresearch.com/jp/reports/global-coal-handling-equipment-market

China: https://www.databridgemarketresearch.com/zh/reports/global-coal-handling-equipment-market

Arabic: https://www.databridgemarketresearch.com/ar/reports/global-coal-handling-equipment-market

Portuguese: https://www.databridgemarketresearch.com/pt/reports/global-coal-handling-equipment-market

German: https://www.databridgemarketresearch.com/de/reports/global-coal-handling-equipment-market

French: https://www.databridgemarketresearch.com/fr/reports/global-coal-handling-equipment-market

Spanish: https://www.databridgemarketresearch.com/es/reports/global-coal-handling-equipment-market

Korean: https://www.databridgemarketresearch.com/ko/reports/global-coal-handling-equipment-market

Russian: https://www.databridgemarketresearch.com/ru/reports/global-coal-handling-equipment-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 1341

Email:- [email protected]

#Coal Handling Equipment Market Size#Coal Handling Equipment Market Shares#Coal Handling Equipment Market Forecast#Coal Handling Equipment Market Growth#Coal Handling Equipment Market Demand

0 notes

Text

Understanding the Changing Landscape of Mine Surveys: Trends, Opportunities, and Challenges

Mine surveying, a critical aspect of the mining industry, has witnessed significant shifts in recent years. These changes are driven by advancements in technology, environmental concerns, and the need for precision and safety. Dolphin Engineers, a key player in the field of mine surveys, offers valuable insights into the evolving trends, the rise of innovative methodologies, and the challenges shaping this domain.

The Rise of Technological Integration

The incorporation of cutting-edge technology has redefined mine surveying practices. From drones to LiDAR systems, technology is streamlining operations, reducing costs, and improving accuracy. Drones, for instance, allow surveyors to access hard-to-reach areas, capturing high-resolution imagery and topographic data. Similarly, LiDAR provides detailed 3D mapping, helping surveyors visualize complex terrains with unparalleled clarity.

Another notable advancement is the integration of Geographic Information Systems (GIS) and Global Positioning Systems (GPS). These tools enable precise data collection, real-time monitoring, and efficient data management. With such capabilities, companies like Dolphin Engineers can deliver results with exceptional accuracy, ensuring projects stay on track.

Environmental and Sustainability Considerations

Environmental awareness has become a significant factor in mine surveying. Companies are now required to minimize their ecological footprint while maintaining operational efficiency. Surveyors play a crucial role in this by using methods that reduce environmental disruption. Techniques such as non-invasive surveying, along with remote sensing technologies, help achieve these goals.

Sustainability initiatives are also influencing mining operations. Accurate surveys ensure that resources are extracted responsibly, aligning with global efforts to protect natural ecosystems. Dolphin Engineers is at the forefront of adopting sustainable practices in their mine survey projects, balancing industrial needs with environmental responsibility.

Challenges in Modern Mine Surveying

Despite technological advancements, the industry faces numerous challenges. Safety remains a primary concern, particularly in underground mines. Complex geological conditions, limited visibility, and hazardous environments require surveyors to rely on robust equipment and techniques.

Moreover, the industry grapples with data management and analysis. The influx of vast amounts of data from various technologies necessitates efficient processing systems. Surveyors must also stay updated with new tools and software, as the fast-paced evolution of technology leaves little room for outdated practices.

Economic fluctuations and regulatory changes further add to the complexity. Mining companies must adapt to varying market demands while adhering to strict legal frameworks. These factors underscore the importance of expertise and adaptability in mine surveying.

Emerging Trends Shaping the Future

The future of mine surveying is set to be defined by automation and artificial intelligence (AI). Automated equipment and AI-driven analytics are transforming how survey data is collected, processed, and interpreted. Autonomous drones, for instance, can conduct surveys without human intervention, enhancing safety and efficiency.

Blockchain technology is another trend gaining traction. By ensuring data integrity and transparency, blockchain can revolutionize data sharing and verification processes in mining operations.

Dolphin Engineers: Pioneering the Way Forward

As the industry navigates these shifts, Dolphin Engineers continues to play a pivotal role in advancing mine survey practices. Leveraging state-of-the-art tools and a commitment to precision, the company addresses challenges head-on, setting benchmarks in safety, accuracy, and sustainability.

By embracing innovation and focusing on client needs, Dolphin Engineers remains a trusted partner in the mining sector. Whether through deploying advanced technologies or adopting eco-friendly practices, the company is dedicated to shaping a future where mine surveys meet the highest standards of excellence.

Conclusion The dynamic field of mine surveying reflects the broader changes in the mining industry. With technological advancements, increased environmental awareness, and evolving methodologies, the landscape is undergoing a transformation. Companies like Dolphin Engineers are leading this journey, combining expertise with innovation to redefine what’s possible in mine surveying. As the industry moves forward, staying adaptable and embracing change will be key to navigating its complexities and seizing new opportunities.

#PrecisionSurveying#MiningSustainability#BlockchainInMining#MiningData#FutureOfMining#MiningTrends#MiningChallenges#AutomationInMining#AIInMining#MiningSafety#EnvironmentalResponsibility#SustainableMining#GISMapping#LiDARTechnology#DroneSurveying#TechnologyInMining#InnovationInMining#DolphinEngineers#MiningIndustry#MineSurveying

0 notes

Text

2 D Materials Market, Market Size, Market Share, Key Players | BIS Research

2D materials are substances that are just a few atoms thick, usually one layer. The most famous 2D material is graphene, discovered in 2004 by physicists Andre Geim and Konstantin Novoselov, which led to a Nobel Prize in Physics in 2010. Graphene is a single layer of carbon atoms arranged in a hexagonal lattice, with incredible mechanical strength, electrical conductivity, and thermal properties.

The 2D materials market is projected to reach $4,000.0 million by 2031 from $526.1 million in 2022, growing at a CAGR of 25.3% during the forecast period 2022-2031.

2 D Materials Overview

2 D Materials focus on addressing the environmental, social, and economic challenges associated with mining activities while ensuring long-term resource availability.

Key components of Sustainable Mining

Reducing energy consumption

Minimizing greenhouse gas emissions

Conserving water

Market Segmentation

1 By Application

• Metallic Minerals

Industrial Metals

Precious Metals

Iron Ore

• Non-Metallic Minerals

Coal

Others

By Process

Underground Mining Surface Mining

By Mining Equipment

• Drill Rigs

• Bolters

• Dozers

• Loaders

By Energy Source

1 Battery

Lithium-Ion Battery

Lead Acid Battery

Others

2 Hydrogen Fuel Cell

3 Bio-Fuel

By Region

North America - U.S., Canada, and Mexico

Europe - Germany, Russia, Sweden, Spain, and Rest-of-Europe

China

U.K.

Download the report and get more information @ 2 D Materials Market

.Major Key Players

• NanoXplore Inc.

• Cabot Corporation

• Thomas Swan & Co. Ltd.

• Ossila Ltd

• ACS Material LLC

Download the sample page click here @ 2 D Materials Market

Demand – Drivers and Limitations

The following are the demand drivers for the global 2D materials market:

• Growing adoption of 2D materials in energy storage • Strong growth of 2D materials in the healthcare industry • Growing demand for transparent conductive films in electronics industry

The market is expected to face some limitations as well due to the following challenges:

• Lack of large-scale production of high-quality graphene • High cost of production

Recent Developments in the Global 2D Materials Market

• In September 2021, Colloids Limited introduced a new infrastructure for customized polymeric materials using its ground-breaking graphanced graphene masterbatch advanced technologies. Due to its extraordinary qualities, graphene has attracted a lot of attention. Additionally, it has exceptional mechanical characteristics as well as superior thermal and electrical permeability.

• In December 2021, Black Swan Graphene Inc. signed a legally enforceable letter of intent to purchase Dragonfly Capital Corp., in a backward merger agreement for $31.5 million. On December 13, 2021, Black Swan Graphene Inc. and Dragonfly Capital Corp. agreed to exchange shares in an opposite merger transaction. Stockholders of Black Swan would then obtain 15.2 consideration shareholdings for every ordinary Black Swan share they own.

Challenges in the 2D Materials Market

Despite the excitement surrounding 2D materials, there are notable challenges that the industry must overcome:

Scalability of Production: Producing high-quality 2D materials at scale remains a challenge. Researchers are exploring various methods, such as chemical vapor deposition (CVD), but the cost and complexity of manufacturing must be addressed for widespread adoption.

Integration into Existing Technologies: For 2D materials to be fully integrated into mainstream applications, they must seamlessly work with existing materials and processes. Compatibility issues with traditional manufacturing methods could slow down the transition.

Cost of Raw Materials and Processing: Currently, the cost of producing 2D materials is relatively high. Developing cost-effective manufacturing techniques is crucial for making these materials economically viable.

The Future of 2D Materials

As the 2D materials market continues to evolve, we are likely to see a wave of disruptive innovations across multiple sectors. With ongoing research, improved production techniques, and increasing investment, these materials could fundamentally reshape industries ranging from electronics to energy and healthcare.

While challenges remain, the unique properties of 2D materials offer unprecedented opportunities for technological advancement. The next few years will be crucial in determining how quickly and effectively these materials can be integrated into real-world applications, but one thing is certain: 2D materials are poised to revolutionize the future of advanced materials.

Key Questions

Q What are the main bottlenecks for scaling up 2D materials, and how can they be overcome?

Q Where do you see the greatest need for additional R&D efforts?

Q How does the supply chain function in the global 2D materials market for end users?

Q What are the key business and corporate strategies of 2D material manufacturers involved in the global 2D materials market?

Q What are the advantages of the emerging 2D materials that are entering the market, and how are they used in various applications?

Q Which applications (by end user) and products (by material type) segments are leading in terms of consumption of the 2D materials market, and which of them are expected to witness high demand growth during 2022-2031?

Q Which regions and countries are leading in terms of consumption of the global 2D materials market, and which of them are expected to witness high demand growth during 2021-2031?

Q What are the most promising opportunities for furthering the efficiency of 2D materials?

Q How has COVID-19 impacted the 2D materials market across the globe?

Q How the semiconductor crisis impacted the 2D materials market?

Conclusion

The 2D materials market is set to grow exponentially as more industries recognize the potential of these atom-thin materials. With ongoing advancements in production techniques, new discoveries of 2D materials, and innovative applications across sectors, the future looks incredibly promising.

0 notes

Text

0 notes

Text

Mining Automation and Its Impact on Workforce Dynamics

Allied Market Research, titled, Global Mining Automation Market by Technique and Type: Global Opportunities Analysis and Industry Forecast, 2017-2023, the mining automation market was valued at $2,193 million in 2016, and is projected to reach at $3,810 million by 2023, growing at a CAGR of 7.9% from 2017 to 2023.

Mining automation involves use of process and software automation, and incorporation of robotic technology in mining vehicles and automation. In 2016, the underground mining segment dominated the market, in terms of revenue, due to increase in investment on automation and infrastructure.

Asia-Pacific was the highest revenue contributor to the golf cart market in 2016, accounting for around 31.41% share, owing to surge in demand for mobility for automation and increase in transition from manual work to automated work.

The report features a competitive scenario of the mining automation market and provides a comprehensive analysis of key growth strategies adopted by major players. Key players operating in the global mining automation market include Autonomous Solution Inc., Atlas Copco, Caterpillar, Hexagon, Hitachi, Komatsu Ltd., Mine site technologies, RPMGlobal Holdings Ltd., Sandvik AB, and Trimble. These players have adopted competitive strategies such as innovation, new product development, and market expansion to boost the growth of the market.

Key Findings of the Mining Automation Market:

The underground mining segment accounted for the highest share in 2016.

Equipment segment generated the highest revenue in 2016.

Asia-Pacific is expected to dominate the market, in terms of market share, during the forecast period

0 notes

Text

Machine à tête de forage en tunnel de type flèche, Prévisions de la Taille du Marché Mondial, Classement et Part de Marché des 12 Premières Entreprises

Selon le nouveau rapport d'étude de marché “Rapport sur le marché mondial de Machine à tête de forage en tunnel de type flèche 2024-2030”, publié par QYResearch, la taille du marché mondial de Machine à tête de forage en tunnel de type flèche devrait atteindre 585 millions de dollars d'ici 2030, à un TCAC de 6.2% au cours de la période de prévision.

Figure 1. Taille du marché mondial de Machine à tête de forage en tunnel de type flèche (en millions de dollars américains), 2019-2030

Figure 2. Classement et part de marché des 12 premiers acteurs mondiaux de Machine à tête de forage en tunnel de type flèche (Le classement est basé sur le chiffre d'affaires de 2023, continuellement mis à jour)

Selon QYResearch, les principaux fabricants mondiaux de Machine à tête de forage en tunnel de type flèche comprennent Sandvik, Sany, XCMG, Antraquip, BBM Group, Famur, Sunward, Mitsui Miike Machinery, CREG, Shanghai Chuangli Group, etc. En 2023, les cinq premiers acteurs mondiaux détenaient une part d'environ 64.0% en termes de chiffre d'affaires.

According to QYResearch, the global key manufacturers of Boom Type Tunnel Roadheader include Sandvik, Sany, XCMG, Antraquip, BBM Group, Famur, Sunward, Mitsui Miike Machinery, CREG, Shanghai Chuangli Group, etc. In 2023, the global top five players had a share approximately 64.0% in terms of revenue.

The boom type tunnel roadheader market is influenced by several key drivers that shape its demand and growth prospects:

1. Infrastructure Development: Large-scale infrastructure projects such as tunnels, metro systems, highways, and underground facilities drive the demand for boom type tunnel roadheaders. These machines are essential for excavating tunnels efficiently and precisely, supporting the construction of transportation networks and utilities.

2. Urbanization and Population Growth: Rapid urbanization worldwide increases the demand for transportation infrastructure, including tunnels for metro lines and road networks. Boom type tunnel roadheaders play a crucial role in creating underground pathways that alleviate traffic congestion and support urban expansion.

3. Mining and Quarrying Activities: In addition to civil construction, boom type roadheaders are used in mining and quarrying operations for excavating rock and minerals. The mining sector's demand for these machines contributes to the overall market growth, particularly in regions with significant mineral resources.

4. Technological Advancements: Ongoing technological advancements in roadheader design enhance their efficiency, reliability, and safety. Innovations in cutting tools, automation, control systems, and telemetry improve excavation precision and reduce downtime, driving adoption among contractors and operators.

5. Environmental Regulations: Increasing environmental regulations necessitate the use of efficient and eco-friendly excavation equipment. Modern roadheaders are designed to minimize emissions, noise levels, and energy consumption, aligning with sustainability goals and regulatory requirements in many regions.

6. Cost Efficiency and Project Economics: Boom type tunnel roadheaders offer cost-effective excavation solutions compared to traditional drilling and blasting methods. They reduce project timelines, labor costs, and material wastage, making them attractive for contractors seeking efficient construction methods and better project economics.

7. Government Investments and Funding: Public and private sector investments in infrastructure projects, including transportation and mining, stimulate the demand for tunneling equipment like roadheaders. Government funding initiatives aimed at improving connectivity and infrastructure resilience further boost market growth.

8. Demand for Underground Space Utilization: Growing interest in utilizing underground spaces for various purposes, such as storage, utilities, and commercial facilities, increases the demand for tunnel excavation equipment. Roadheaders enable efficient and safe construction of underground structures, supporting diverse applications.

In summary, the boom type tunnel roadheader market is driven by infrastructure development, urbanization trends, mining activities, technological advancements, environmental considerations, cost efficiency benefits, government investments, and the expanding utilization of underground spaces. These drivers collectively propel the demand for roadheader equipment across various global markets.

À propos de QYResearch

QYResearch a été fondée en 2007 en Californie aux États-Unis. C'est une société de conseil et d'étude de marché de premier plan à l'échelle mondiale. Avec plus de 17 ans d'expérience et une équipe de recherche professionnelle dans différentes villes du monde, QYResearch se concentre sur le conseil en gestion, les services de base de données et de séminaires, le conseil en IPO, la recherche de la chaîne industrielle et la recherche personnalisée. Nous société a pour objectif d’aider nos clients à réussir en leur fournissant un modèle de revenus non linéaire. Nous sommes mondialement reconnus pour notre vaste portefeuille de services, notre bonne citoyenneté d'entreprise et notre fort engagement envers la durabilité. Jusqu'à présent, nous avons coopéré avec plus de 60 000 clients sur les cinq continents. Coopérons et bâtissons ensemble un avenir prometteur et meilleur.

QYResearch est une société de conseil de grande envergure de renommée mondiale. Elle couvre divers segments de marché de la chaîne industrielle de haute technologie, notamment la chaîne industrielle des semi-conducteurs (équipements et pièces de semi-conducteurs, matériaux semi-conducteurs, circuits intégrés, fonderie, emballage et test, dispositifs discrets, capteurs, dispositifs optoélectroniques), la chaîne industrielle photovoltaïque (équipements, cellules, modules, supports de matériaux auxiliaires, onduleurs, terminaux de centrales électriques), la chaîne industrielle des véhicules électriques à énergie nouvelle (batteries et matériaux, pièces automobiles, batteries, moteurs, commande électronique, semi-conducteurs automobiles, etc.), la chaîne industrielle des communications (équipements de système de communication, équipements terminaux, composants électroniques, frontaux RF, modules optiques, 4G/5G/6G, large bande, IoT, économie numérique, IA), la chaîne industrielle des matériaux avancés (matériaux métalliques, polymères, céramiques, nano matériaux, etc.), la chaîne industrielle de fabrication de machines (machines-outils CNC, machines de construction, machines électriques, automatisation 3C, robots industriels, lasers, contrôle industriel, drones), l'alimentation, les boissons et les produits pharmaceutiques, l'équipement médical, l'agriculture, etc.

0 notes

Text

Underground Hard Rock Equipment Market Insights and Global Outlook 2024-2030

Global Info Research announces the release of the report “Global Underground Hard Rock Equipment Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030” . This report provides a detailed overview of the market scenario, including a thorough analysis of the market size, sales quantity, average price, revenue, gross margin and market share.The report provides an in-depth analysis of the competitive landscape, manufacturer’s profiles,regional and national market dynamics, and the opportunities and challenge that the market may be exposed to in the near future. Global Underground Hard Rock Equipment market research report is a comprehensive analysis of the current market trends, future prospects, and other pivotal factors that drive the market. According to our (Global Info Research) latest study, the global Underground Hard Rock Equipment market size was valued at US$ million in 2023 and is forecast to a readjusted size of USD million by 2030 with a CAGR of %during review period. This report is a detailed and comprehensive analysis for global Underground Hard Rock Equipment market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2024, are provided.

Market Segmentation Underground Hard Rock Equipment market is split by Type and by Application. For the period 2019-2029, the growth among segments provides accurate calculations and forecasts for consumption value by Type, and by Application in terms of volume and value. Market segment by Type: Underground Loaders、Underground Excavators、Underground Transport Systems、Others Market segment by Application:Tunnel Engineering、Mining、Geological Exploration、Others Major players covered: Atlas Copco、Caterpillar、CMM Equipments、DOVE、Epiroc、FAMUR、Fibo Intercon、Kawasaki、Komatsu、Liebherr、Maccaferri、MACLEAN、Putzmeister、Sandvik、TITAN The content of the study subjects, includes a total of 15 chapters: Chapter 1, to describe Underground Hard Rock Equipment product scope, market overview, market estimation caveats and base year. Chapter 2, to profile the top manufacturers of Underground Hard Rock Equipment, with price, sales, revenue and global market share of Underground Hard Rock Equipment from 2019 to 2024. Chapter 3, the Underground Hard Rock Equipment competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast. Chapter 4, the Underground Hard Rock Equipment breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030. Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030. Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Underground Hard Rock Equipment market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030. Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis. Chapter 13, the key raw materials and key suppliers, and industry chain of Underground Hard Rock Equipment. Chapter 14 and 15, to describe Underground Hard Rock Equipment sales channel, distributors, customers, research findings and conclusion. Our Market Research Advantages: Global Perspective: Our research team has a strong understanding of the company in the global Underground Hard Rock Equipment market.Which offers pragmatic data to the company. Aim And Strategy: Accelerate your business integration, provide professional market strategic plans, and promote the rapid development of enterprises. Innovative Analytics: We have the most comprehensive database of resources , provide the largest market segments and business information. About Us: Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provide market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

The Platinum Mining Market: A Comprehensive Analysis

Introduction

Platinum, often referred to as the "white gold," is one of the most valuable and versatile metals on Earth. From its use in catalytic converters to its role in jewelry and electronics, platinum's significance cannot be overstated. This article delves deep into the platinum mining market, exploring its history, key players, environmental impacts, and future trends.

History of Platinum Mining

Early Discoveries

The story of platinum begins in ancient Egypt, where it was used in small quantities for decorative purposes. However, it wasn't until the 18th century that platinum was recognized as a distinct metal. The Spanish conquistadors discovered it in South America, dismissing it as an impurity in gold and silver mining.

Evolution of Mining Techniques

Platinum mining has come a long way since those early days. Initially, the extraction process was rudimentary, relying heavily on manual labor. Today, advanced technologies and machinery have revolutionized the industry, making platinum mining more efficient and sustainable.

Global Platinum Reserves

Major Platinum-Producing Countries

South Africa dominates the global platinum production, accounting for over 70% of the world's supply. Other significant producers include Russia, Zimbabwe, and Canada. These countries boast extensive platinum reserves, with South Africa's Bushveld Complex being the most notable. Buy the Full Report for More Insights into the Global Platinum Market Forecast, Download A Free Report Sample

Estimated Reserves by Region

The global platinum reserves are estimated to be around 70,000 metric tons, with the majority concentrated in South Africa. Russia and Zimbabwe also have substantial reserves, contributing to their status as leading producers.

Mining Methods

Open Pit Mining

Open pit mining is a common method for extracting platinum, particularly in areas where the ore is close to the surface. This technique involves removing large quantities of soil and rock to access the valuable platinum deposits beneath.

Underground Mining

For deeper platinum deposits, underground mining is the preferred method. This involves creating tunnels and shafts to reach the ore, which is then brought to the surface for processing.

Hybrid Mining Techniques

Some mines employ a combination of open pit and underground mining techniques, optimizing the extraction process based on the specific characteristics of the ore body.

Technological Advancements in Platinum Mining

Modern Equipment

The introduction of modern equipment has significantly improved the efficiency and safety of platinum mining. High-powered drills, automated loaders, and advanced processing plants are just a few examples of the technology in use today.

Automation in Mining

Automation is transforming the mining industry, with automated machinery and robotics reducing the need for human intervention. This not only enhances safety but also boosts productivity and precision in mining operations.

Environmental Technologies

Environmental technologies are becoming increasingly important in platinum mining. Innovations such as water recycling systems, dust control measures, and energy-efficient machinery help minimize the environmental footprint of mining activities.

Key Players in the Platinum Mining Industry

Leading Companies

The platinum mining industry is dominated by a few key players. Companies like Anglo American Platinum, Impala Platinum, and Norilsk Nickel are among the largest and most influential in the market.

Market Share Analysis

These leading companies control a significant share of the global platinum market, with Anglo American Platinum alone accounting for nearly 40% of the world's production. The concentration of market power among these players shapes the dynamics of the industry.

Economic Impact of Platinum Mining

Contribution to National Economies

Platinum mining is a vital component of the economies of producing countries. In South Africa, for instance, the platinum sector contributes significantly to GDP, export earnings, and employment.

Job Creation and Community Development

Mining operations often bring jobs and infrastructure development to local communities. These benefits, however, must be balanced against potential social and environmental costs.

Environmental Concerns and Sustainability

Impact of Mining Activities

Platinum mining, like all forms of mining, has environmental consequences. These include habitat destruction, water pollution, and greenhouse gas emissions. Managing these impacts is a key challenge for the industry.

Sustainable Practices and Innovations

To address environmental concerns, many mining companies are adopting sustainable practices. These include reducing water and energy consumption, rehabilitating mined land, and investing in cleaner technologies.

Regulatory Frameworks

Governments play a crucial role in regulating the environmental impact of platinum mining. Strict environmental laws and regulations ensure that mining companies adhere to sustainable practices.

Market Trends and Forecasts

Current Market Trends

The platinum market is influenced by a variety of factors, including industrial demand, geopolitical dynamics, and technological advancements. Recent trends indicate a growing demand for platinum in emerging applications such as hydrogen fuel cells.

Future Market Projections

Analysts predict steady growth in the platinum market over the next decade. The metal's unique properties and diverse applications ensure its continued relevance and value.

Factors Influencing Market Dynamics

Several factors influence the platinum market, including supply chain disruptions, fluctuations in commodity prices, and changes in environmental regulations. Understanding these dynamics is crucial for stakeholders in the industry.

Demand and Supply Dynamics

Key Drivers of Demand

The primary drivers of platinum demand are the automotive, industrial, and jewelry sectors. In particular, the use of platinum in catalytic converters for vehicles is a major demand driver.

Supply Chain Challenges

Supply chain challenges, such as labor strikes, geopolitical tensions, and logistical issues, can impact the availability of platinum. These challenges often lead to fluctuations in market prices and supply stability.

Platinum Applications and Uses

Industrial Uses

Platinum is widely used in industrial applications due to its resistance to corrosion and high melting point. It is essential in the production of catalytic converters, electronics, and chemical processing equipment.

Jewelry and Investment

Platinum's rarity and lustrous appearance make it a popular choice for jewelry. Additionally, it is viewed as a valuable investment asset, often compared to gold and silver.

Emerging Applications

Emerging applications for platinum include its use in hydrogen fuel cells and renewable energy technologies. These applications highlight the metal's versatility and potential for future growth.

Investment Opportunities in Platinum Mining

Investment Trends

Investing in platinum mining can be lucrative, with many opportunities in both established and emerging markets. Trends indicate a growing interest in sustainable and ethically sourced platinum.

Risks and Rewards

While there are significant rewards in platinum mining investments, there are also risks. These include market volatility, regulatory changes, and operational challenges. Investors must carefully assess these factors before committing.

Challenges in Platinum Mining

Technical Challenges

Technical challenges in platinum mining include the depth and complexity of ore bodies, as well as the need for advanced extraction and processing techniques.

Economic and Political Risks

Economic and political risks, such as fluctuating commodity prices and unstable political environments, can affect the profitability and feasibility of platinum mining projects.

Case Studies

Successful Platinum Mines

Case studies of successful platinum mines, such as the Mogalakwena mine in South Africa, provide valuable insights into best practices and strategies for success in the industry.

Lessons Learned

Lessons learned from these case studies emphasize the importance of innovation, sustainability, and strategic planning in achieving long-term success in platinum mining.

Conclusion

The platinum mining market is a dynamic and complex industry with significant economic, environmental, and social implications. As demand for platinum continues to grow, driven by both traditional and emerging applications, the industry must navigate challenges and opportunities to ensure sustainable and profitable growth. By adopting innovative technologies and sustainable practices, platinum mining can continue to play a vital role in the global

0 notes

Text

Smart Mining Market Size, Share & Industry Trends 2024-2032

IMARC Group’s report titled “Smart Mining Market Report by Type (Underground Mining, Surface Mining), Component (Hardware, Software, Services), Automated Equipment (Excavator, Robotic Truck, Driller and Breaker, Load Haul Dump, and Others), and Region 2024-2032“. The global smart mining market size reached US$ 12.9 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 49.0…

View On WordPress

0 notes

Text

HVC Market: An Explainer on Widening Applications

Given the infrastructure space, the budgetary allocation, industry CAPEX, and policy reforms have spearheaded investments in various projects in the past few years. The European Commission declared grants for 135 transport projects under the Connecting Europe Facility. Such projects will guarantee an increase in demand for all types of high voltage cables to meet energy demands among the growing population. As per Triton’s analysis, the global high voltage cable market is expected to garner revenue worth $59.80 billion by 2030, growing at a CAGR of 5.52% during the forecast period 2023-2030.

Equipped with various conductors and insulators, HVCs are designed to transmit electricity over long distances without power losses. This benefit has elevated their adoption in various sectors, including infrastructure and renewable energy.

Rising Applications: Bridging the Growth Gap

We know that HVCs are expansively employed for high voltage energy transmission; however, their application is not limited to infrastructure. The vertical sector in the studied market includes renewable energy, infrastructure, and industrial. Let’s dive into each category to understand their role in the market’s expansion.

Renewable Energy: While there are several renewable energy sources, investments in solar and wind energy are by far at their peak. As per the Global Wind Energy Council, wind farms are estimated to generate around 536 GW of global power over the next 5 years. A sizable number of HVCs will be required to connect offshore projects to the main grid line. In this regard, submarine cables will be employed for offshore projects, while overhead cables will find application in onshore projects.

Regional Focus: Several European governments are supporting clean energy projects, with Germany leading over other nations. By 2050, the nation’s energy transition plan aims to generate 80% of electricity via renewable sources. To achieve this target, the nation is set to upgrade its high voltage power transmission networks. Further, in the Asia-Pacific, China leads in renewable energy installations, attaining a capacity of approximately 1020 GW in 2021. These factors are thus expected to offer lucrative opportunities for market development.

Industrial: Triton’s analysis of the given market by industrial vertical includes categories like mining, oil & gas, power & utilities, chemical & petroleum, and others. Estimates indicate the power & utility subsegment holds the largest share at a CAGR of 4.23% in the category. Underground and overhead cables have gained prominence in power utility, manufacturing, and mining, while the submarine is used in the oil & gas industry. The robust demand for HVCs is supported by the rising focus on installing power generation plants to support growing operations.

Regional Focus: Industrialization and government initiatives across the UK, Germany, France, and Spain have elevated the adoption of high voltage cables. Large-scale HVCs are employed for excavation projects for powering on-site machines. As per our analysis, the natural gas sector is anticipated to expand greatly. In South East Europe, the Gas Corridor pipeline infrastructure has delivered the first 10 billion cubic meters of gas as of March 2022. The Baltic Pipe Project is another project that connects gas reservoirs in Israel and Cyprus to Greece. These mega projects have widened the scope of the Europe HVC market.

Infrastructure: The HVC market is supported by various commercial and residential construction projects. The commercial category captures a majority of shares in the infrastructure segment. Several nations in Asia-Pacific, the Middle East, and Latin America have undertaken upgradation projects from rail signaling to network infrastructure. Overhead and underground cables are widely deployed in big commercial spaces with the capacity to have their substations. Additionally, the rising demand to upgrade broadband services and the advent of the 5G network has influenced network providers to upgrade infrastructure, ultimately driving the high voltage cable market.

Regional Focus: Canada declared its plan to phase out coal-fired electricity by 2030, with the provinces of Alberta, Saskatchewan, and British Columbia, setting ambitious energy targets. The government aims to invest around $350 billion in electricity infrastructure by 2030, soaring demand for various power equipment, including high voltage cables. Such developments are projected to open avenues for HVC manufacturers in North America.

Growth Outlook: Competitive Analysis

Given the rising applications of high voltage cables, there is intense competition among contenders. In recent years, urbanization, high power consumption, and investment in emerging nations have influenced players to acquire more contracts or engage in product launches to gain a higher market share.

NKT Cable, in January 2022, acquired Ventcroft Ltd to add its fire-resistant cable technology to the product line and expand in the European power cable market.

In September 2022, NKT Cable introduced low-carbon copper for the 320 kV HVDC cables to lower carbon footprint, delivered to Dogger Bank C in the North Sea.

Tratos partnered with Enertechnos in 2019 to develop an innovative cable to tackle the UK's energy loss.

In retrospect, population growth and industrialization have elevated the demand and production of HVCs across sectors. However, the rising efforts to limit global temperature below 2 °C under the Paris Agreement are expected to fuel the deployment of HVCs for clean energy development projects, ultimately driving the high voltage cable market on an additional growth trajectory.

FAQs:

Q1) What are the different types of high voltage cables?

Submarine, underground, and overhead are different HV cable types.

Q2) What factors are fueling high voltage cable adoption?

The growing infrastructure activities, high power demand, and development in emerging nations fuel the adoption of high voltage cables globally.

0 notes

Text

Copper Mining Market Analysis, Brands Statistics and Overview by Top Manufacturers 2030

The market research study titled “Copper Mining Market Share, Trends, and Outlook | 2030,” guides organizations on market economics by identifying current Copper Mining market size, total market share, and revenue potential. This further includes projections on future market size and share in the estimated period. The company needs to comprehend its clientele and the demand it creates to focus on a smaller selection of items. Through this chapter, market size assists businesses in estimating demand in specific marketplaces and comprehending projected patterns for the future.

The Copper Mining market report also provides in-depth insights into major industry players and their strategies because we understand how important it is to remain ahead of the curve. Companies may utilize the objective insights provided by this market research to identify their strengths and limitations. Companies that can capitalize on the fresh perspective gained from competition analysis are more likely to have an edge in moving forward.

With this comprehensive research roadmap, entrepreneurs and stakeholders can make informed decisions and venture into a successful business. This research further reveals strategies to help companies grow in the Copper Mining market.

Market Analysis and Forecast

This chapter evaluates several factors that impact on business. The economics of scale described based on market size, growth rate, and CAGR are coupled with future projections of the Copper Mining market. This chapter is further essential to analyze drivers of demand and restraints ahead of market participants. Understanding Copper Mining market trends helps companies to manage their products and position themselves in the market gap.

This section offers business environment analysis based on different models. Streamlining revenues and success is crucial for businesses to remain competitive in the Copper Mining market. Companies can revise their unique selling points and map the economic, environmental, and regulatory aspects.

Report Attributes

Details

Segmental Coverage

Mining Technique

Open-pit Mining

Underground Mining

Application

Equipment manufacturing

Building and Construction

Infrastructure and Transportation

Others

Geography

North America

Europe

Asia Pacific

and South and Central America

Regional and Country Coverage

North America (US, Canada, Mexico)

Europe (UK, Germany, France, Russia, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, Australia, Rest of APAC)

South / South & Central America (Brazil, Argentina, Rest of South/South & Central America)

Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA)

Market Leaders and Key Company Profiles

Freeport-McMoRan

Glencore

Amerigo Resources Ltd.

BHP

Codelco

African Copper Plc

Southern Copper

Hindustan Copper Ltd

First Quantum Minerals Ltd.

Rio Tinto.

Other key companies

Our Unique Research Methods at The Insight Partners

We offer syndicated market research solutions and consultation services that provide complete coverage of global markets. This report includes a snapshot of global and regional insights. We pay attention to business growth and partner preferences, that why we offer customization on all our reports to meet individual scope and regional requirements.

Our team of researchers utilizes exhaustive primary research and secondary methods to gather precise and reliable information. Our analysts cross-verify facts to ensure validity. We are committed to offering actionable insights based on our vast research databases.

Strategic Recommendations

Strategic planning is crucial for business success. This section offers strategic recommendations needed for businesses and investors. Forward forward-focused vision of a business is what makes it through thick and thin. Knowing business environment factors helps companies in making strategic moves at the right time in the right direction.

Summary:

Copper Mining Market Forecast and Growth by Revenue | 2030

Market Dynamics – Leading trends, growth drivers, restraints, and investment opportunities

Market Segmentation – A detailed analysis by product, types, end-user, applications, segments, and geography

Competitive Landscape – Top key players and other prominent vendors

About Us:

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

0 notes

Text

Mining Automation Market Forecast: Growth, Trends, and Opportunities

The global mining automation market size is expected to reach USD 8.64 billion by 2030, registering a CAGR of 7.3% from 2023 to 2030, according to a new report by Grand View Research, Inc.

The increasing demand for accuracy and productivity required during mining activities is the high-impact rendering driver for the industry. The growing adoption of automated mining is attributed to the advantages associated with automated systems. For instance, in January 2022, Hexagon AB, one of the eminent players in digital reality solutions combining sensors, independent technology, and software programs, acquired Minnovare, one of the prominent players in drilling technology that enhances the cost, speed, and accuracy of drilling underground.

The initiative aims to strengthen and accelerate Hexagon AB’s underground roadmap and strengthen the drill and blast portfolio. The industry witnesses the adoption of drones as a step towards the evolution of unmanned and aerial data collection technology at mining sites. The automated drone system is poised to become an essential strategic part of the future of mining. For instance, in June 2020, Caterpillar Inc. acquired Marble Robots Inc. The initiative was aimed at expanding Robotization and autonomy strategy and demonstrating its commitment to the coming generation of job site results. Structure on its leadership in independent mining, the organization aims to work and bring scalable results to fulfill the changing needs of construction, chase, artificial, and waste diligence.

Furthermore, the upcoming concept in mining operations is the use of central or virtual control room that monitors several mines in distant sites from a single location. The virtual control room is expected to facilitate benchmarking and comparison of identical processes at different plants. For instance, in January 2022, Accenture, a services-based company that provides a wide range of services in interactive, strategy, and consulting technology and operations, collaborated with Celonis. This data processing company sells Software as a Service (SaaS) to enhance business processes, and it has formed a partnership to work in process mining.

Gather more insights about the market drivers, restrains and growth of the Mining Automation Market

Mining Automation Market Report Highlights

• The mineral mining application segment will register the fastest CAGR over the forecast period

• Increased mineral exploration activities globally are expected to boost the segment's growth

• The implementation & maintenance services segment held a significant market share in 2022

• In terms of equipment automation, autonomous trucks dominated the industry in 2022

• Retrofitting the mining equipment with automated technology is expected to contribute to the growth of the equipment automation segment considerably

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

• The global drone charging station market size was estimated at USD 0.43 billion in 2023 and is expected to grow at a CAGR of 6.5% from 2024 to 2030.

• The global data protection as a service market size was valued at USD 22.05 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 25.9% from 2024 to 2030.

Mining Automation Market Segmentation

Grand View Research has segmented the global mining automation market based on solution, application, and region:

Mining Automation Solution Outlook (Revenue, USD Million, 2018 - 2030)

• Software Automation

• Services

o Implementation & Maintenance

o Training

o Consulting

• Equipment Automation

o Autonomous Trucks

o Remote Control Equipment

o Teleoperated Mining Equipment

Mining Automation Application Outlook (Revenue, USD Million, 2018 - 2030)

• Metal Mining

• Mineral Mining

• Coal Mining

Mining Automation Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o Canada

o U.S.

• Europe

o Germany

o U.K.

• Asia Pacific

o Australia

o China

o India

o Japan

• Latin America

o Brazil

o Mexico

• Middle East & Africa

Order a free sample PDF of the Mining Automation Market Intelligence Study, published by Grand View Research.

#Mining Automation Market#Mining Automation Market Analysis#Mining Automation Market Report#Mining Automation Market Size#Mining Automation Market share

0 notes

Text

Underground Mining Equipment market Size, Growth, Future Plans and Global Trends by Forecast 2030

The Insight Partners latest offering, titled “Underground Mining Equipment Market Size and Share Analysis to 2030,” provides comprehensive insights for startups and big market players. The report covers industry performance, risk factors, growth determinants, economics of cost, and ROI streams. It combines qualitative and primary research methods, making it an essential product for companies, investors, and business strategists aiming to excel in the Underground Mining Equipment market in a projected timeframe. Underground Mining Equipment market has experienced dynamic transformations in recent years, anticipated to remain an investible domain for investors in the projected time. The market is propelled by consumer preferences, regulatory parameters, and advancements in technology. Concurrently, the surge in automation has favored Underground Mining Equipment market share expansion. Advancements in manufacturing technologies have made the Underground Mining Equipment market viable and accessible, which is further expected to contribute to market growth.

0 notes

Text

Sustainable Mining Solutions Market, Market Size, Market Share, Key Players | BIS Research

Sustainable mining solutions are approaches and practices that aim to reduce the negative environmental, social, and economic impacts of mining activities while promoting long-term benefits. These solutions focus on minimizing resource depletion, reducing greenhouse gas emissions, managing waste responsibly, and preserving biodiversity.

The Sustainable Mining Solutions Market was valued at around $2,159.8 Million in 2022 and is expected to reach $12,371.0 Million by 2033, at a CAGR of 18.97% from 2022 to 2033.

Sustainable Mining Solutions Overview

Sustainable mining solutions focus on addressing the environmental, social, and economic challenges associated with mining activities while ensuring long-term resource availability.

Key components of Sustainable Mining

Reducing energy consumption

Minimizing greenhouse gas emissions

Conserving water

Market Segmentation

1 By Application

• Metallic Minerals

Industrial Metals

Precious Metals

Iron Ore

• Non-Metallic Minerals

Coal

Others

By Process

Underground Mining Surface Mining

By Mining Equipment

• Drill Rigs

• Bolters

• Dozers

• Loaders

By Energy Source

1 Battery

Lithium-Ion Battery

Lead Acid Battery

Others

2 Hydrogen Fuel Cell

3 Bio-Fuel

By Region

North America - U.S., Canada, and Mexico

Europe - Germany, Russia, Sweden, Spain, and Rest-of-Europe

China

U.K.

Download the report and get more information @ Sustainable Mining Solutions Market

Key Applications

Energy Efficiency and Renewable Energy Integration

Water Management

Waste Management and Circular Economy

Low Impact Mining Techniques

Community Engagement and Social Responsibility

.Major Key Players

Sandvik AB

Komatsu Ltd.

XCMG Mining Machinery Co. Ltd.

Hitachi Construction Machinery Co., Ltd

And many others

Download the sample page click here @ Sustainable Mining Solutions market

Demand – Drivers and Limitations

The following are the demand drivers for the global sustainable mining solutions market:

• Incentives and Support from Governments • Lower Operating Cost Over Time

The market is expected to face some limitations as well due to the following challenges:

• High Initial Costs • Lack of Infrastructure to Support Sustainable Technologies

Recent Developments

• In April 2023, XCMG Machinery unveiled a range of new electric mining equipment products, broadening its application scope to encompass the complete cycle of mining operations. This development underscores XCMG’s dedication to providing comprehensive solutions for the mining industry, further enhancing efficiency and effectiveness in mining operations.

• In March 2023, CharIN, in collaboration with ICMM, inaugurated a new mining taskforce. This initiative signifies a concerted effort to advance sustainable practices and innovation within the mining industry, further promoting the goals of both organizations in advancing responsible mining operations.

Future Outlook

1 Technological Innovations

Emerging technologies will play a pivotal role in advancing sustainable mining practices. The use of automation, artificial intelligence (AI), and the Internet of Things (IoT) is expected to optimize resource extraction, reduce waste, and lower energy consumption.

2. Decarbonization and Renewable Energy

The mining sector will continue to shift toward decarbonization by incorporating renewable energy sources such as solar, wind, and hydropower.

3 Circular Economy and Waste Minimization

The move toward a circular economy will gain traction, with mining companies increasingly focusing on waste reduction, material recycling, and reprocessing of mine tailings.

Key Questions

Q What are the main factors driving the demand for hybrid memory cubes and high-bandwidth memory?

Q What are the latest technological advancements in hybrid memory cubes and the high- bandwidth memory market?

Q What is the bottleneck around the adoption of hybrid memory cubes and high-bandwidth memory across different regions and countries?

Q How does the supply chain function in the global hybrid memory cube and high-bandwidth memory market?

Q What are the major patents filed by the companies active in the global hybrid memory cube and high-bandwidth memory market?

Q What are the strategies adopted by the key companies to gain a competitive edge?

Conclusion

In conclusion, sustainable mining solutions are essential to ensuring the long-term viability of the industry while minimizing environmental degradation and enhancing social and economic benefits. By adopting innovative technologies, promoting efficient resource use, and integrating renewable energy sources, the mining sector can reduce its ecological footprint. Furthermore, fostering collaboration between governments, local communities, and mining companies is crucial for creating transparent, equitable, and responsible practices. Sustainable mining not only protects ecosystems and biodiversity but also contributes to the well-being of local populations, creating a pathway for a more responsible and resilient future for both the environment and industry.

#Sustainable Mining Solutions Market#Sustainable Mining Solutions Report#Sustainable Mining Solutions Industry

0 notes

Text

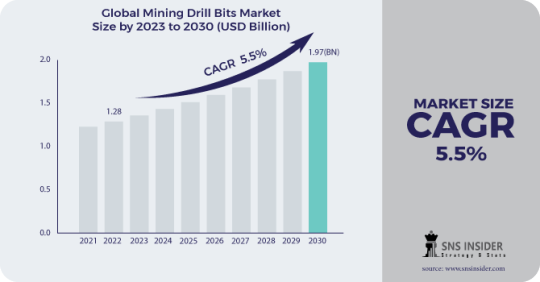

Understanding the Scope: Mining Drill Bits Market Analysis and Forecast for 2031

Global Mining Drill Bitsmarket research provides a comprehensive overview of fundamental data on market volume, industry growth potential, and business structure. All this contributes to the growth of the market. In addition, the study provides details on technology investments over the projected time horizon and a unique perspective on global demand in many of the categories studied. Mining Drill Bits market research helps clients better understand industry challenges and opportunities. Based on geography, global market research provides up-to-date information on consumer technology advances and growth potential.

Ask For Sample Report Here @ https://www.snsinsider.com/sample-request/1091

The study on global Mining Drill Bitsmarket provide in-depth analysis of future technologies, RDD projects, and new products. The study looks at all the major innovations and breakthroughs that are expected to have a significant impact on global market growth in the coming years. Likewise, the studies look at all sectors in different geographic areas and provide a cross-sectional analysis of the global economy in terms of demand forecasts. It also describes the many variables, constraints and opportunities in the market that will almost certainly impact business growth over the next few years.

Segmentation View

BY TYPE

Rotary bits

Fixed cutter bits

Roller cones bits

DTH Hammer bits

Others

BY MATERIAL

PDC Diamond

Tungsten carbide

Steel

Others

BY SIZE

Below 8 inches

8 to11 inches

Above 11 inches

BY APPLICATION

Surface mining

Underground Mining

By Company

The major key players are Rockmore International, Western Drilling Tools Inc, CATTERPILLAR INC., Robit Plc,Epiroc AB, Sandvik AB, Brunner & Lay Inc., Xiamen Prodrill Equipment Co. Ltd., Mitsubishi Materials Corporation, MICON-Drilling GmbH, Boart Longyear, DATC Group, Changsha Heijingang Industrial Co., Ltd.

The segmentation analysis section of the Mining Drill Bits market research focuses on past and future industry dynamics, business development, and challenges faced by the global vendors and consumers. Based on a comprehensive model of primary research and distribution, this article explores global markets at the national and regional levels, focusing on the major global suppliers. Mining Drill Bits market research and regional retail and distribution assessments using state-of-the-art methods.

Competitive Scenario

The report provides detailed industry competitive research and an overview of Porter's Five Forces model to help clients understand the competitive environment of leading global vendors in the Mining Drill Bitsmarket. This lengthy publication also provides a comprehensive review and summary of each research chapter. In order to provide viewers of this survey with an accurate picture of the global Mining Drill Bits industry, this report provided a highly competitive environment and product offerings from major vendors spread across multiple locations. The survey includes the latest analysis of the market forecast for the forecast period.

The Mining Drill Bitsresearch report explores four levels of detail, including market share analysis of major companies, business analysis (industry trends), supply chain analysis, and brief industry profiles. The study also provides an overview of the business environment, high growth markets, and high growth countries, differences in relevant industry, business factors and constraints.

Buy This Report Here @ https://www.snsinsider.com/checkout/1091

Report Conclusion

The report will help market participants to revisit their strategies and make necessary changes to stay in firm position in the competitive market.

0 notes

Text

Tunnel Boring Machine Market by Product, Technology, and Application 2027

Tunnel boring machines are pivotal in excavating tunnels across diverse geological formations. Mainly utilized in coal mines and tunnel construction, TBMs are witnessing a surge in demand owing to the expanding railway and highway infrastructure projects globally. The tunnel boring machine market is poised for substantial growth, driven by its increasing utilization in water management, oil and gas pipelines, and hydropower initiatives.

As underground construction gains momentum worldwide, the demand for tunnel boring machines is skyrocketing, expected to maintain a robust growth trajectory in the coming years. These machines, renowned for their ability to excavate tunnels with circular cross-sections through varying rock and soil types, are indispensable in modern infrastructure development.

Moreover, the hard rock mining sector is increasingly adopting tunnel boring machines to expedite mine development processes and achieve accelerated rates of advance in civil tunnel construction. This trend is set to further propel the growth of the tunnel boring machines market during the forecast period, underlining their indispensable role in shaping the infrastructure landscape.

Download Updated Insights with Sample Report @ https://www.alliedmarketresearch.com/request-sample/5200

The tunnel boring machines market size was valued for $5.47 billion in 2019, and is expected to reach $7.55 billion by 2027, growing at a CAGR of 6.0% from 2020 to 2027. In 2019, Asia-Pacifc region dominated the global market, in terms of revenue, accounting for about 48.99% share of the global market, followed by Europe.

The tunnel boring machine market is poised for growth, driven by several key factors:

Government Investments: Increased government funding for infrastructural development projects worldwide is a significant driver. As nations invest in expanding their transportation networks, tunnel boring machines play a pivotal role in creating efficient underground passages.

Infrastructure Development: Developing countries like India and China are leading the charge in road and railway infrastructure development. For instance, Shanghai's substantial investment of $38 billion in a new infrastructure project from 2020 to 2022 underscores the growing demand for tunnel boring machines.

Mining Industry Adoption: The mining industry's increased adoption of tunnel boring machines further propels market growth. These machines are instrumental in accessing valuable mineral deposits safely and efficiently.

Despite these promising drivers, the tunnel boring machine market faces certain challenges: